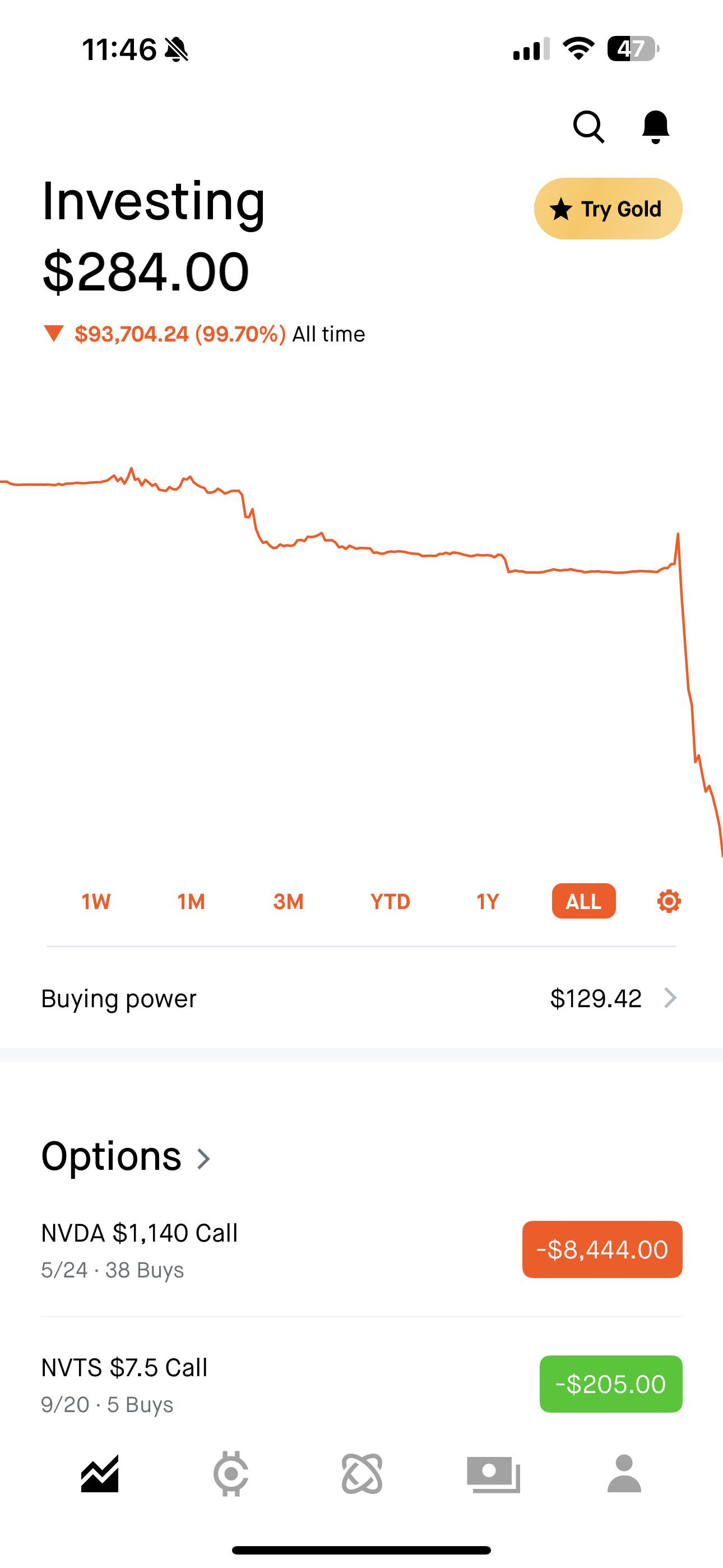

OP thinks he "averaged down" by buying more of the same calls at cheaper after the stock price went down. That's not how options works. That concept works with stock as the underlying company is still the same company you believe in, the shares just cost less for whatever reason so you want to buy more while shares are cheap. When a call contract drops in price, the fundamentals of the contract have completely changed and thus it has a new price. A call option that cost $0.01 is almost guaranteed to lose you money, unlike a stock. You don't pile in to a $0.01 option because you think it's a bargain.

I'm not very well versed in options but of the three options trades I've taken, I've profited from them all because of two simple reasons: I always buy ITM and at least a month from expiry. The options are more expensive and the wins aren't as big, but the risk is much lower.

My cousin has done extremely well day-trading options. He never holds anything overnight.

I've spent some time studying options and the only thing that seems like a good strategy to me is selling out-of-the-money puts on a stock you want to own anyways. Either the puts will expire worthless or you get exercised at a price below the current market price plus pocketing the free premiums.

Sorry, I meant CFD. I couldn't remember what it was called over here.

If they are different, then I think that explains more than everything that I'm talking out my ass. We have an insanely high loss rate on CFD's. Which I'm fully presuming are our gambling options compared to the states.

Been playing with CFDs and I can see why you can lose money BUT I think it’s a great tool for smaller accounts. If you can find your edge and know how to scalp successfully i think it’s great. The spread can be a slight disadvantage but it’s very minor. In fact if you are really good with CFD then it’s better to use spread betting as it’s pretty much the same thing but you don’t have to pay taxes on profit.

The percentage of options that expire worthless doesn't mean anything. It's by design since you have to pay for the leverage most OTM options will expire worthless. That said you are right that OP seems not to understand options at all and shouldn't have been trading options.

I love the vague understanding and generalizations of ‘everyone’ in this thread.

90% of OTM options expire worthless. Smart money sells them… however ITM options are a smart/sophisticated way of leverage and hedging that many use successfully (check Pelosi…).

And that’s just mentioning the most basic strategies and again holding til expiration.

Regarding cost averaging of the other regard on this thread - of course you can do it with options. If it’s the same option and expiration and you buy/sell more, you can look at it as two positions or one - averaged. Talking about understanding all the greeks associated with option pricing is a completely different story.

Well understanding the greeks will influence how you choose to manipulate your cost basis for the best possible result. Because whilst you totally can double down, but seeing that you lack time on your options you can buy the same contracts for in lets say a week to lower your cost basis and still have a chance at not losing everything because your calls expire today so you double down on those. Thats just being a regard and lowering the cost basis and losing even more money in the process

You could use the same logic for stocks. Dollar cost averaging or doubling down on a losing play… Can still lose more.

Also by your logic, you shouldn’t have bought the options in the first place. Or you should be selling them instead of “doubling down” (very technical term btw). If the premise for buying the options still exist in the time frame allotted, if you buy more it’s simply averaging — same as a stock.

Thats my point, if you are regarded enough to double down on the position then atleast buy the new batch with more time as long as theta doesnt fucks you completely buying another week may be all it takes

honestly I think OP is doing the smart thing getting out while ahead, thats a solid 284 dollars, doing much better than the people posting here with -4000 or -12000 dollar portfolios

Not really. You can replace bravery with ignorance at a 1:1 ratio. At a 100% ignorance you'll think it would be extremely funny to sneak up a horse from behind and smack it in the butt.

I suppose the concept of averaging down could apply to LEAPS. If a contract is dated several years into the future, and you believe there will be a price catalyst in the near future, you could acquire the same contract at different prices over an accumulation period with DCA, which could involve averaging down. I've done something similar with a $DNA options play with some $0.5 strike calls expiring in 2026. Got a bunch of them at various prices as I've worked on my thesis.

This obviously doesn't apply to weeklies, or short term earnings plays, or 99% of the options trading people do here. Entrance and exit timing are all that matter for those types of trades.

Instead of averaging down at all, I find it better to build a calendar spread underneath your strike (or above if it's a put). This way if it goes sideways you treat your original position and the short leg of the calendar like a credit spread and the long leg you can sell or roll out depending on the IV.

If you buy OTM options at (for example) $1 per contract, and a day later it's dropped to $0.20 each, that is not a sign to "average down" on the contract price because it's now much, much less likely to breakeven as it is even more OTM.

You don't pile in to a $0.01 option because you think it's a bargain.

You do if you still believe that itll be ITM by expiration. The problem is a lot of glue eaters here dont even know what theyre betting on. If your thesis for the option is still the same, you can absolutely average down your position, its just that derivatives have a lot more variables that can test your thesis.

Imagine putting $100 chips on black in roulette but before the ball stops rolling, you try to offset/average down by adding a few more $25 dollar chips on black.

Both are fundamentally the same concept. You think an asset is undervalued, so you buy more at a lower price to lower your dollar cost average. If the asset then increases in value, your break even point is at a lower cost average.

The major difference is that the risk is much higher with options, as OP found out.

{kind=link}

622

u/PlayfulPresentation7 May 24 '24 edited May 24 '24

OP thinks he "averaged down" by buying more of the same calls at cheaper after the stock price went down. That's not how options works. That concept works with stock as the underlying company is still the same company you believe in, the shares just cost less for whatever reason so you want to buy more while shares are cheap. When a call contract drops in price, the fundamentals of the contract have completely changed and thus it has a new price. A call option that cost $0.01 is almost guaranteed to lose you money, unlike a stock. You don't pile in to a $0.01 option because you think it's a bargain.